The U.S. property market 2026 is entering a phase defined by income stability, disciplined underwriting, and measured capital flows.

If you sit in enough cross-border investment meetings, one thing becomes clear: the tone has changed.

Three or four years ago, conversations about U.S. real estate often centered on acceleration — price growth, migration spikes, bidding wars. Today, the discussion is quieter and far more analytical. Investors are less interested in “what might surge” and more focused on “what is likely to hold.”

That shift matters. It explains a large part of why international capital is once again circling U.S. property — not because it expects dramatic appreciation, but because it sees something increasingly rare in global real estate: income that looks defensible.

And in 2026, defensible income is valuable.

The Yield Comparison Is No Longer Subtle

Across many global gateway cities, rental yields have compressed over the past decade. In parts of Western Europe and major Asia-Pacific hubs, gross yields frequently sit in the low single digits once acquisition costs are factored in.

By comparison, several U.S. metropolitan areas — particularly outside the most expensive coastal corridors — continue to offer materially higher rental yields. In a number of secondary cities, gross yields in the mid-single digits remain achievable, sometimes higher depending on asset type and local conditions.

According to recent national housing data releases in early 2026, rent growth has moderated from post-pandemic peaks but remains positive in many regions, while home price growth has slowed. That combination has quietly improved yield mathematics in select markets.

For institutional allocators, that is not a minor detail.

Recent market releases from the National Association of Realtors show that while transaction activity has normalized compared to pandemic peaks, broad-based price declines remain limited across most regions. At the same time, rental occupancy levels in several mid-sized metropolitan areas have held steady, reinforcing income durability even as price growth moderates.

When capital is deployed at scale, even a one- or two-percentage-point yield differential reshapes portfolio projections over a 10-year horizon.

This is not about chasing upside. It is about protecting return assumptions.

Is the U.S. Property Market 2026 Still Attractive for Income Investors?

The short answer is yes — but for different reasons than in prior cycles. In the U.S. property market 2026, investors now build return expectations less on rapid appreciation and more on income durability. That shift is subtle, but structurally important.

What Experienced Investors Are Actually Watching

In conversations with market participants — asset managers, cross-border advisors, and private equity analysts — a consistent theme emerges: underwriting discipline has tightened.

Instead of assuming aggressive rent growth, investors are stress-testing deals against:

-

Flat rent scenarios

-

Mild vacancy increases

-

Slower population inflows

These are not catastrophic assumptions. They are realistic ones.

If a property still produces acceptable cash flow under conservative assumptions, it moves forward. If it requires perfect conditions to perform, it is usually passed over.

This approach reflects experience earned through recent volatility. Policy guidance over the past year from the Federal Reserve has reinforced a higher-for-longer interest rate environment. While that has cooled speculative buying and compressed leverage-driven strategies, it has also reduced overheating risk in several markets — a dynamic many long-term investors quietly view as constructive.

Global investors are not abandoning risk, but they are pricing it more carefully.

The U.S. market’s advantage here is structural transparency. Transaction data, rent comparables, and regulatory frameworks are generally easier to evaluate than in many other jurisdictions. That clarity lowers informational risk — a factor often underestimated outside institutional circles.

Single-Family Rentals: From Opportunistic to Core Allocation

Single-family rental housing has matured significantly over the past decade. What was once a fragmented space dominated by small landlords now includes large, professionally managed platforms.

For foreign investors, this evolution matters. It reduces operational uncertainty and creates scalable entry points.

The demand story is less sensational than in 2021, but arguably more stable. Household formation continues, affordability challenges persist in many metros, and not all renters are positioned to transition into homeownership quickly.

From an income perspective, this creates a broad tenant base. Stability in occupancy — even with moderate rent growth — supports the kind of predictable cash flow that conservative capital values.

It is not glamorous. It is functional.

Multifamily: The Quiet Workhorse

Multifamily remains central to many international allocations. What has changed is the criteria.

Investors are looking beyond headline cities and asking practical questions:

-

Is local employment diversified, or dependent on one sector?

-

How aggressive is the current construction pipeline?

-

Are rent increases supported by wages, or speculation?

Markets with moderate, sustainable expansion tend to rank higher than those that experienced extreme surges followed by sharp corrections.

Recent research briefings from CBRE continue to note that rental resilience remains strongest in markets where supply pipelines are measured rather than aggressive. That nuance matters, particularly for cross-border investors who prioritize downside protection over rapid upside.

In 2026, a market that grows slowly but consistently often looks more attractive than one that oscillates between extremes.

National multifamily vacancy rates have hovered in the mid-6% range into early 2026, according to industry tracking reports. While slightly above the unusually tight levels seen during the post-pandemic surge, this level remains well below historical stress thresholds.

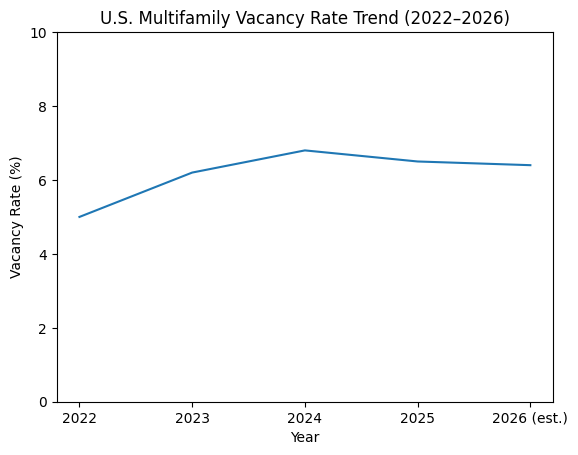

For income-focused investors, that distinction matters — moderate vacancy does not undermine cash flow the way double-digit vacancy rates would.

The regional picture is even more revealing. Take Texas: according to the latest estimates from the U.S. Census Bureau, the state added more than 470,000 residents in the most recent annual update — one of the strongest gains nationwide. That kind of demographic momentum does not always appear immediately in quarterly rent data, but over time it quietly supports absorption and occupancy stability.

Investors view mid-6% vacancy rates as evidence of market balance rather than weakness. Within the broader U.S. property market 2026, it signals balance — a reversion from unusually tight conditions toward a more sustainable equilibrium.

Currency and Capital Structure: Managed Exposure

When foreign buyers ignore currency risk, exchange-rate swings can erode the returns they ultimately realize.

However, seasoned investors rarely treat currency as a binary obstacle. Many hedge exposure partially, finance locally within the United States, or incorporate exchange assumptions directly into underwriting models.

What ultimately supports allocation decisions is the relative stability of rental cash flow. Even when currency movements fluctuate, predictable income can soften overall volatility.

In this sense, U.S. rental property functions less as a speculative trade and more as a portfolio stabilizer.

Secondary Markets: Less Noise, More Durability

While coastal markets still draw global attention, experienced investors shift capital toward secondary metros in search of durability.

Cities such as Columbus, Indianapolis, and Charlotte are not immune to economic cycles, but they often exhibit steadier rent-to-price relationships and lower entry thresholds.

From an investor’s standpoint, these markets offer room for yield without requiring heroic assumptions about future growth. Population data published by the U.S. Census Bureau continues to show net migration into several secondary metropolitan areas, particularly in regions with diversified employment bases. That ongoing movement supports rental demand beyond short-term market cycles.

There is a practical logic at work here. When risk tolerance declines globally, capital tends to migrate toward assets that are understandable and defensible. Secondary U.S. markets increasingly fit that description.

Why This Strengthens the Broader Investment Thesis

The renewed global interest in U.S. property is sometimes framed as a simple “flight to safety.” That description is incomplete.

What appears to be happening in 2026 is more nuanced. Investors are conducting relative comparisons. When evaluated against alternatives — whether overheated prime cities or less transparent emerging markets — U.S. rental housing often presents a balanced profile:

-

Measurable income

-

Transparent legal structure

-

Scalable investment platforms

-

Deep tenant demand

These characteristics do not eliminate risk — no market can. But they allow investors to measure and price that risk with greater confidence.

Global investors constructing diversified portfolios value structural clarity more than excitement.

What has changed most noticeably is not just the numbers, but the conversations behind them. In prior cycles, spreadsheets often justified optimism. In 2026, they justify restraint. And restraint, in real estate, is rarely a bad sign.

A Personal Observation from the Market

In recent months, investors have chosen discipline over exuberance. Deals that close are rarely based on aggressive narratives. They are supported by spreadsheets that assume modest growth and realistic occupancy.

This restraint, paradoxically, may be one of the healthiest signs for the U.S. property market in 2026.

When capital returns without speculation dominating the conversation, it suggests conviction built on fundamentals rather than momentum.

And that conviction is precisely what reinforces the central argument of the broader thesis: international investors are not returning to U.S. property out of nostalgia or fear of missing out. They are returning because, when income, transparency, and long-term structure are weighed together, the numbers — and the experience — still make sense.

When viewed through this lens, the renewed global interest in American real estate is easier to understand. The appeal is not built on dramatic price forecasts but on comparative positioning within a volatile world.

In the U.S. property market 2026, investors shift capital toward income durability, structural transparency, and disciplined underwriting — and away from pure momentum.

For a broader look at why international capital is reallocating toward U.S. property again — and how macro, structural, and institutional factors combine to support that shift — see our full analysis in Why Investors Worldwide Are Turning to U.S. Property Again.

{kind=link}