Not long ago, global investors were chasing the same U.S. cities everyone recognized — New York, Los Angeles, San Francisco. In 2026, that pattern is quietly changing.

It’s no longer just about buying in the most famous cities. With interest rates remaining elevated under the policy stance of the Federal Reserve, investors are placing greater emphasis on income stability rather than short-term price acceleration.

In fact, many experienced investors are doing the opposite — looking beyond the obvious, toward markets where growth is steady, demand is durable, and entry prices still leave room for yield.

By 2026, that shift has become more visible. Capital is still flowing into U.S. real estate, but it’s moving with more selectivity — and increasingly toward cities that combine demographic momentum with manageable risk.

This shift becomes clearer when viewed alongside broader market conditions, as explored in our analysis of the U.S. property market in 2026, where supply, pricing, and investor behavior are evolving in parallel.

Market briefings from CBRE Research continue to highlight stronger relative performance in high-growth secondary markets compared to traditional coastal hubs.

Why Secondary Cities Are Getting More Attention

For years, gateway markets like New York or San Francisco dominated international investment flows. That hasn’t disappeared entirely, but the calculus has changed.

High entry prices, compressed yields, and slower rent growth have pushed many investors to reassess where value actually exists.

Part of this shift is also driven by changing borrowing conditions, as explored in our analysis how interest rates are reshaping U.S. property investment in 2026.

At the same time, several mid-sized metropolitan areas have quietly strengthened their fundamentals:

- Population growth

- Job diversification

- More balanced housing supply

- Lower acquisition costs

Recent population estimates from the U.S. Census Bureau continue to show migration trends shifting toward these regions, reinforcing long-term housing demand.

These are not explosive markets — and that’s exactly why they matter. For long-term investors, stability often outperforms volatility.

For those evaluating the best U.S. cities for property investment in 2026, the focus has clearly shifted toward balance rather than hype.

Austin, Texas — Growth With Volatility Awareness

Austin continues to attract attention, and not without reason. The city has benefited from sustained in-migration, a strong technology sector, and a relatively young workforce.

Over the past few years, rapid construction activity has introduced more supply into the market, temporarily moderating rent growth.

That has made some investors more cautious, but not absent. From a longer-term perspective, Austin still represents a growth market. The key is entry timing and underwriting discipline. Investors who account for short-term supply pressure often see opportunities where others only see cooling momentum.

Over the past year, Austin saw rent growth normalize to around 2–3% annually after a period of aggressive expansion, reflecting a market that is cooling but not collapsing.

From a practical standpoint, this is where many investors start to slow down their decision-making — not because the opportunity disappears, but because timing begins to matter more than momentum.

Dallas–Fort Worth, Texas — Scale and Consistency

If Austin represents growth with fluctuation, Dallas–Fort Worth represents scale. The metro area has one of the largest population bases in the country and continues to expand.

Economic activity is diversified across industries, from logistics to finance to technology.

For investors, this translates into something less dramatic but more dependable: consistent rental demand across multiple submarkets.

Yields may not spike, but they tend to hold. And for institutional capital, that consistency is often more valuable than peak performance.

The Dallas–Fort Worth metro added more than 150,000 residents in a single year, according to recent estimates from the U.S. Census Bureau, reinforcing one of the deepest rental demand bases in the country.

Charlotte, North Carolina — Quiet Financial Expansion

Charlotte does not always dominate headlines, but it continues to strengthen as a financial and banking hub. Job growth in finance and related sectors supports a stable renter base.

At the same time, housing costs remain lower than in traditional financial centers.

The result is a market where rent levels are supported by income, rather than speculation. That balance reduces the risk of sharp corrections — something global investors increasingly prioritize.

Charlotte has recorded job growth in the range of 2–3% annually, particularly in finance and professional services, supporting steady rental absorption.

Tampa, Florida — Migration-Driven Demand

Tampa has seen significant population inflows over the past several years, driven by both domestic migration and lifestyle shifts.

That growth has supported rental demand, particularly in multifamily housing. While some areas have experienced increased construction, demand has remained resilient enough to absorb new supply over time.

Investors watching Tampa tend to focus on long-term demographic trends rather than short-term rent fluctuations.

Tampa’s population has grown by roughly 2% per year in recent estimates, keeping rental demand resilient despite increased construction activity.

Indianapolis, Indiana — Yield Over Headlines

Not every attractive market is high-growth. Indianapolis represents a different kind of opportunity — one built on affordability and yield rather than rapid appreciation.

Entry prices remain relatively accessible, allowing for stronger rental returns compared to many coastal markets.

For investors focused on cash flow, markets like Indianapolis often serve as portfolio stabilizers.

They rarely attract headlines, but in many portfolios, they quietly do the heavy lifting.

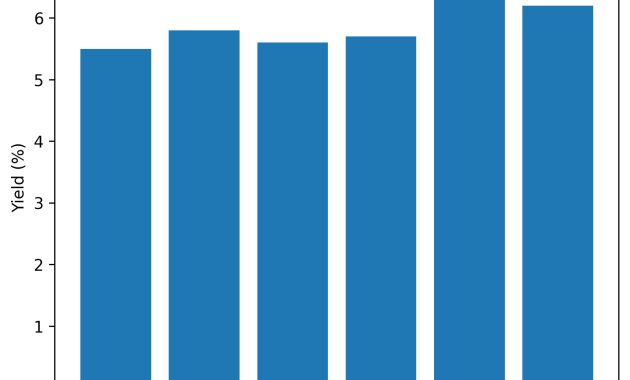

Gross rental yields in Indianapolis often range between 6% and 7%, significantly higher than most coastal markets.

Columbus, Ohio — Demographics and Education Base

Columbus continues to benefit from a mix of education, healthcare, and government employment.

That combination creates a steady demand profile that is less sensitive to economic swings than single-industry cities. Population growth, while not explosive, has been consistent enough to support housing absorption.

For investors, this translates into lower volatility — and in the current environment, that is increasingly valuable.

Columbus has maintained steady population growth of around 1–1.5% annually, supported by its education and healthcare sectors.

What These Cities Have in Common

Despite their differences, these markets share several characteristics that attract global capital.

For investors comparing the best U.S. cities for property investment in 2026, these shared fundamentals often matter more than short-term momentum.

- Population inflows or stable demographic trends

- Diverse employment bases

- Housing affordability relative to income

- Manageable supply pipelines

None of these factors guarantee outperformance. But together, they create conditions where risk is easier to assess — and therefore easier to price.

A More Selective Kind of Capital

One of the defining traits of 2026 is not where investors are going, but how they are making decisions.

There is less urgency, less speculation, and far more scrutiny. Deals are evaluated under conservative assumptions. Markets are compared, not chased.

In that context, cities that offer balance — not extremes — are gaining attention.

Closing Perspective

The map of U.S. property investment is not shrinking. It is becoming more detailed.

Global investors are no longer concentrating capital in a handful of high-profile cities. They are spreading it across markets that offer different forms of value: growth, yield, stability, or a combination of the three.

Understanding where capital is moving is not just about geography. It is about recognizing how investment priorities have changed.

For a broader perspective on why international capital is increasingly reallocating toward U.S. real estate, see our full analysis in Why Investors Worldwide Are Turning to U.S. Property Again, where we break down the structural forces behind this shift.

In 2026, the shift is clear — not toward what looks exciting, but toward what continues to work when the market settles. In the end, the best U.S. cities for property investment in 2026 are not necessarily the most visible — but the most resilient.

{kind=link}